Who can join the Sacco?

- Any individual/person(s) from all occupations can join i.e. Employed, Self-employed, Clergy among others.

What is the meaning of BOSA?

- BOSA is an acronym of Back Office Service Activity. It refers to those activities (products & services) offered in the back office.

What is the meaning of FOSA?

- FOSA is an acronym of Front Office Service Activity. It refers to those activities (products & services) offered in the banking division of the SACCO.

How can I get my statement?

- Members are encourage to register in members’ portal through the link https://portal.imarishasacco. co.ke:42443/Login/member or send a request to diaspora@ imarishasacco.co.ke

How much dividends do I get every year?

- Every financial year (1st Jan to 31st Dec), the SACCO declare dividends on share capital and interest on deposits based on the business performance.

Is my investment Secure/ Insured?

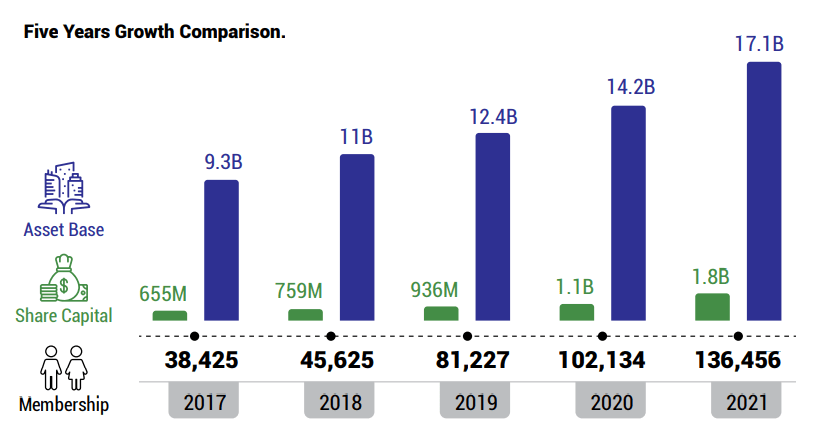

- Yes, the members’ investment is insured and very secure as the deposit has been reinsured. Since inception in 1978, there has been an upward trajectory growth in membership (currently over 140,000 members), share capital is at Kshs. 1.67 Billion and currently the Asset base is over Kshs. 18 Billion, an indication of a very stable SACCO.

Do you have an office in Nairobi?

- Yes, we have an office/branch located in Upperhill, Longonot road, Embarkment Plaza.

What is the Minimum Monthly contribution?

- 1, 600/= is the minimum monthly contribution which is made up of Kshs.1, 200/= shares/deposits & Kshs.400/= that goes to the members welfare.

What is the Kshs.400/= welfare monthly contribution?

- The welfare amount is mandatory for all members. The contribution is pool into a sinking fund that assist in the following ways:

- Upon demise of a member, the bereaved family is send a last expense/consolation amount of Kshs.150, 000/=.

- A deceased member deposits is doubled and paid to the nominee.

- In case a deceased member had a loan balance, the sinking fund is used to write-off the loan balance. • Assist members to pay their medical bills after exhausting their personal health insurance and government managed health insurance allotment. The welfare support members who are referred for specialized treatment.

- Members who are diagnosed with cancer are given an upkeep of Kshs.300, 000/=.

A deceased member deposits is doubled and paid to the nominee?

- In case a deceased member had a loan balance, the sinking fund is used to write-off the loan balance.

- Assist members to pay their medical bills after exhausting their personal health insurance and government managed health insurance allotment. The welfare support members who are referred for specialized treatment.

- Members who are diagnosed with cancer are given an upkeep of Kshs.300, 000/=.

What is the difference between share capital and Sacco savings/deposits?

- Savings/Deposits are refundable while Share Capital is nonrefundable but transferrable to a nominee or another member.

- Share capital earn dividends while savings/deposits earn interest.

- Shares are never used as a loan security while deposits may be used as loan security.

- Members are not permitted to borrow against share capital as Shares are never used as a loan security while deposits may be used as loan security.

Who is a nominee?

- “A nominee” means a person appointed by a member to inherit the shares, deposits and other interests in the Sacco society upon the death of that member.

How is share Capital transferred?

- With the approval of the board, a member who wish to exit the SACCO may at any time transfer shares to another member but not to a non-member. Such transfers must be in writing by both the member exiting and the member buying the shares.

Can I buy shares?

- First, you have to enroll as a member to be able to buy shares and by purchasing shares, you become a shareholder in the SACCO.

- Acquisition of shares is done through direct remittance (bank transfer, Cash deposit etc) or monthly contribution (Check-off or Standing Orders). An enrolling or active member may also buy from a member who is exiting the SACCO.

When can I apply for the loan and how do I get it?

- A member can apply for a loan after an active KYC relationship period of six (6). The loan shall be credited to the member’s FOSA account and can be accessed via M-Imarisha App, USSD code, Visa card, bank transfers, cheques & over the counter withdrawals.

What are some of the loan products for diaspora members?

- Ughaibuni Loan, Homeland Loan, Nguvu Loan, Diaspo Loan, Asset Finance & Mortgage.

- Do all the loan products require cosigner?

- Most loan products require an active member to cosign, however, there are some products that only require collateral or cosigner and chattels. 19. How do I send monies to my account in IMARISHA?

- Sendwave, Worldremit etc, bank transfer, standing orders, direct debits or any other diaspora remitting channels.